Dsip Cost Volume Form Using Cost-Volume-Profit Models for Sensitivity Analysis

Introduction: When a Single Assumption Breaks Your Profit Forecast

In my hands-on work with pricing and budgeting, I’ve seen teams build a cost forecast that looks “correct” on paper—then watch actual results miss the plan by weeks. The usual culprit isn’t math errors; it’s sensitivity to assumptions like selling price, unit variable cost, and volume. That’s exactly where a cost-volume-profit model becomes valuable: it turns your profit logic into a controllable experiment.

This article explains how to use a cost-volume-profit (CVP) model for sensitivity analysis, using the dsip cost volume form (a structured way to translate assumptions into profit outcomes). By the end, you’ll know how to test which inputs matter most and how to present results clearly to decision-makers.

Core Idea: The dsip cost volume form (How CVP Becomes a Sensitivity Tool)

CVP models link three drivers—cost, volume, and profit—through a small set of relationships. When you run sensitivity analysis, you’re not changing the business; you’re changing the inputs to see how outcomes react.

1) The DSIP view (from assumptions to profit)

In practical terms, I use a dsip cost volume form that forces clarity:

- D (Demand/Volume): units sold (or production/sales volume)

- S (Sales price per unit): selling price assumptions

- I (Costs): variable cost per unit and fixed costs

- P (Profit outcome): operating profit (or loss)

This framing is useful because it mirrors how assumptions are negotiated in real organizations: sales sets price, operations estimates volume, finance owns cost structure, and leadership wants to know what profit would look like under each scenario.

2) The CVP logic you’ll repeatedly use

A standard CVP structure looks like this:

- Contribution Margin per Unit = Sales price per unit − Variable cost per unit

- Total Contribution Margin = Contribution margin per unit × Volume

- Operating Profit = Total contribution margin − Fixed costs

- Break-even Volume = Fixed costs ÷ Contribution margin per unit

Once you can compute profit from those inputs, sensitivity analysis becomes straightforward: you vary one input at a time (or multiple inputs together) and measure the change in profit or break-even volume.

How to Perform CVP Sensitivity Analysis (Step-by-Step)

In the field, the biggest mistake I see isn’t misunderstanding CVP—it’s doing sensitivity analysis without a decision question. Before you change numbers, decide what you’re trying to prevent or enable.

Step 1: Identify the decision and the metrics

Examples of decision questions I’ve worked on:

- “How much profit do we lose if price drops by 3%?”

- “What unit cost increase can we tolerate before we miss the target break-even date?”

- “If volume is uncertain, what probability of loss are we taking?”

Then choose the output metric(s) to report—commonly operating profit, break-even volume, or required volume to hit a profit target.

Step 2: Build a baseline dsip cost volume form

Start with your most defensible estimates for:

- Sales price per unit

- Variable cost per unit

- Fixed costs

- Expected sales/production volume

In my experience, I always document where each number came from (vendor quotes, historical run rates, last-quarter actuals). That documentation is what makes the analysis trustworthy to stakeholders later.

Step 3: Choose sensitivity “ranges” that reflect reality

Sensitivity only matters if the tested changes are plausible. For example:

- Price sensitivity might reflect discounting or competitive pressure (e.g., −2% to +1%).

- Variable cost sensitivity might reflect material volatility or labor efficiency (e.g., +0% to +10%).

- Volume sensitivity might reflect demand uncertainty (e.g., −15% to +15%).

I’ve found that using ranges tied to actual observed variability (from past quarters or supplier history) dramatically improves credibility.

Step 4: Run “one-way” sensitivity first, then combine drivers

One-way sensitivity answers: “Which single input changes profit the most?”

Multi-way scenarios answer: “What happens if multiple things move together?” For instance, price may fall while variable cost rises—an uncomfortable but realistic combination.

Step 5: Report results in a way leadership can use

Don’t just list numbers. Tell a story with implications:

- What assumption drives profit most?

- At what break-even point does risk become unacceptable?

- What operational levers can realistically respond (cost reduction, pricing action, volume initiatives)?

Example: Translating Cost, Volume, and Profit into Sensitivity Outputs

Below is a compact example of how you might present dsip cost volume form results. Imagine a product with:

- Sales price per unit: $50

- Variable cost per unit: $30

- Fixed costs: $120,000

- Baseline volume: 8,000 units

Contribution margin per unit is $20. Baseline operating profit is:

Profit = ($20 × 8,000) − $120,000 = $160,000 − $120,000 = $40,000.

Common sensitivity outputs to compute

- Profit under alternative volume: vary volume and recompute profit

- Break-even volume: fixed costs ÷ contribution margin per unit

- Profit under alternative price: update contribution margin per unit, then profit

- Profit under alternative variable cost: same logic, different driver

Simple sensitivity table (one-way)

| Scenario | Sales Price | Variable Cost | Volume | Operating Profit |

|---|---|---|---|---|

| Baseline | $50 | $30 | 8,000 | $40,000 |

| Price −5% | $47.50 | $30 | 8,000 | $20,000 |

| Variable cost +5% | $50 | $31.50 | 8,000 | $28,000 |

| Volume −10% | $50 | $30 | 7,200 | $24,000 |

What matters is not only the changes but the ranking: which input creates the biggest profit swing? In many real projects, price and variable cost dominate because they change contribution margin, which multiplies across volume.

Where CVP Sensitivity Analysis Fits Best (And Where It Doesn’t)

CVP sensitivity analysis is powerful, but it’s not magic. In my day-to-day consulting, I set clear boundaries so teams don’t misapply the model.

Best use cases

- Pricing and discounting decisions: test how margin changes propagate to profit.

- Budgeting with uncertain volume: understand downside before commitments lock in.

- Cost reduction planning: quantify the profit impact of variable cost improvements and fixed cost leverage.

- New product planning: evaluate break-even assumptions early.

Limitations to acknowledge

- Linearity assumptions: CVP typically assumes stable variable costs and a constant selling price per unit across the relevant range.

- Fixed cost behavior: fixed costs may shift (step costs), especially with capacity changes.

- Product mix effects: if multiple products exist, contribution margin depends on mix, not just volume.

- Time dynamics: CVP is often static for a period; it doesn’t fully capture learning curves or demand seasonality.

When stakeholders understand these limits, they trust the analysis more—even when it reveals uncomfortable outcomes.

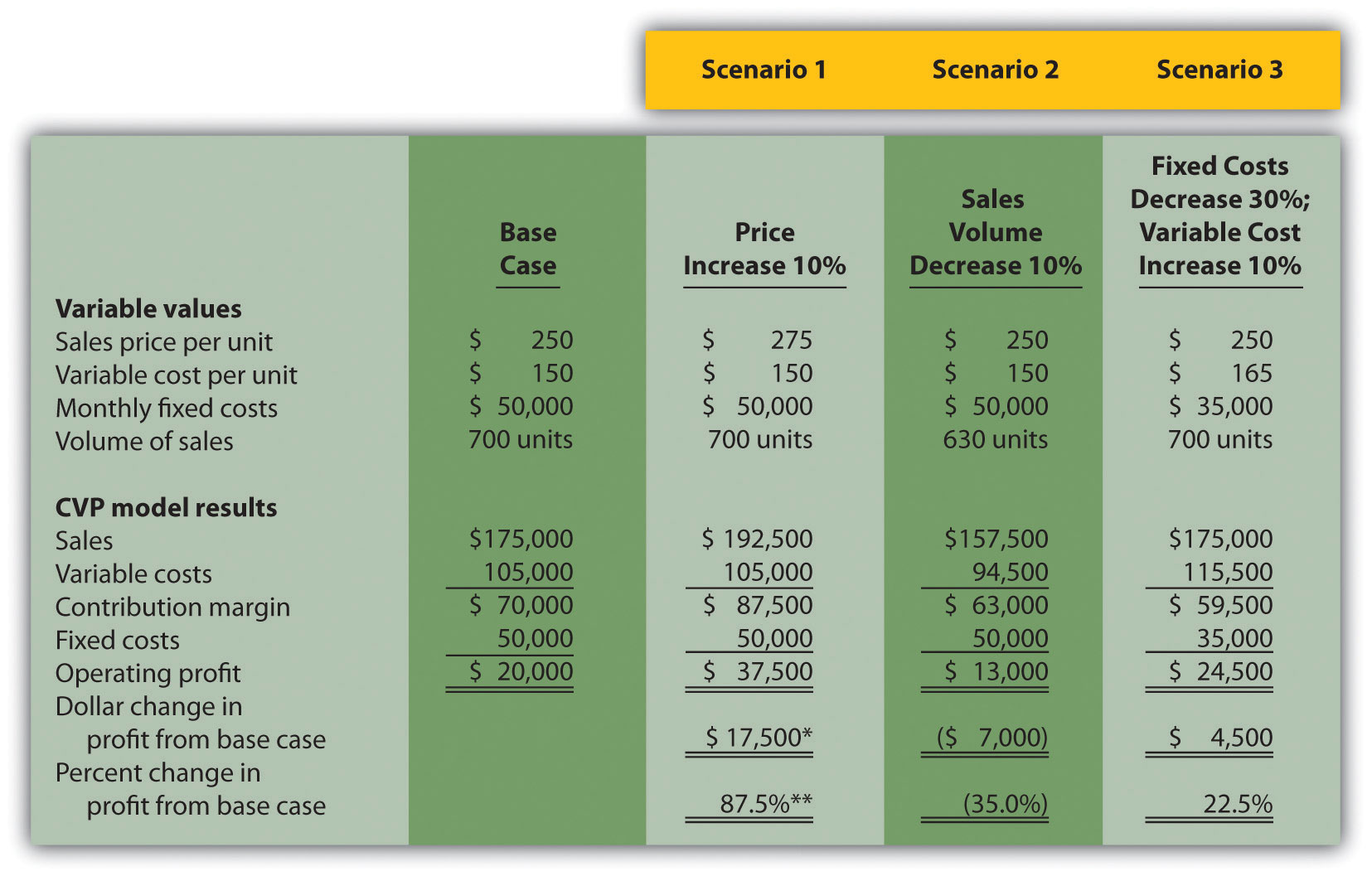

Visual Support: Use a Clear Model Diagram for Stakeholder Buy-In

Stakeholders absorb sensitivity results faster with a simple visual that connects inputs to profit. Here’s an image you can incorporate into a model documentation page or internal briefing deck to reinforce the structure of the CVP workflow.

FAQ

What does “dsip cost volume form” mean in practical terms?

It’s a structured way to map assumptions to outcomes: D (volume), S (sales price), I (costs—variable and fixed), leading to P (profit). It helps you run sensitivity tests systematically and explain “what changes profit most” clearly.

How do I choose which assumptions to test in sensitivity analysis?

Start with inputs that (1) are uncertain, (2) are controllable or decision-relevant, and (3) directly affect contribution margin. In many teams, price and variable cost changes create the largest profit swing because they scale with volume.

Should I run one-way or multi-way sensitivity?

Begin with one-way sensitivity to identify the biggest drivers. Then run multi-way scenarios for realism—especially combinations that stress the business (e.g., lower price with higher variable costs).

Conclusion: Turn CVP into a Decision-Ready Sensitivity Experiment

Using cost-volume-profit models for sensitivity analysis helps you move from “a forecast we hope is right” to “a decision framework we can manage.” With the dsip cost volume form, you systematically connect volume, price, and cost assumptions to profit outcomes, then test plausible ranges to uncover the true drivers of risk.

Next step: Build a baseline CVP for your key product or business line, run one-way sensitivity on price, variable cost, and volume, and present a simple table ranking which assumption changes operating profit the most—then decide what action you’d take for the worst credible scenario.

Discussion